Quick Summary:

- AI cybersecurity for UAE fintech must cover customer data, AI models, app logic, APIs, cloud hosting, and vendor tools.

- AI adoption is safer when each use case has a risk tier, a named owner, an audit trail, and a human review level.

- IBM reports that 63% of organizations lack AI governance policies, which makes shadow AI a direct security risk.

- UAE fintech apps must treat PDPL, GDPR, ISO 27001, ISO 42001, NIST, OWASP, and CBUAE-aligned controls as design requirements.

AI cybersecurity solutions for UAE fintech enable the adoption of AI without increasing cyber risk. This can be made possible by building AI security into data, models, APIs, vendor integrations, and human approval workflows before launch.

Why AI Cybersecurity Solutions Matter for UAE Fintech Companies in 2026

AI cybersecurity can improve fraud detection, onboarding, remittance support, risk scoring, and customer service. It can also expose personal data, create unfair decisions, automate risky actions, and give attackers new ways to manipulate financial workflows.

That is why AI cybersecurity solutions are no longer a technical add-on. For a fintech founder, CTO, CISO, or compliance head in Dubai or Abu Dhabi, AI security is now part of product strategy.

IBM’s 2025 Cost of a Data Breach Report puts the global average breach cost at USD 4.4 million. The same report found that 97% of organizations with an AI-related security incident lacked proper AI access controls, while 63% lacked AI governance policies.

The risk is not AI alone. The risk is AI without governance.

- A fintech chatbot can expose support history, whereas a fraud model can block the wrong account.

- A remittance AI agent can process sensitive data through an unapproved vendor.

- A credit scoring model can create bias or explainability risk.

For UAE fintech companies, secure AI adoption means every AI feature must answer four questions:

- What data does the AI use?

- What decision does the AI influence?

- Who can override the AI?

- What evidence can be shown to a regulator, auditor, or enterprise client?

What Do AI Cybersecurity Solutions For Fintech in UAE Involve?

AI security in fintech is the practice of protecting AI systems, data flows, model decisions, and automated workflows from misuse, manipulation, privacy exposure, and cyberattack.

Traditional cybersecurity protects networks, apps, accounts, APIs, and infrastructure. AI security adds model-specific risks.

These include prompt injection, data poisoning, hallucinated outputs, model drift, sensitive information disclosure, insecure plugins, and excessive autonomy.

OWASP lists prompt injection, insecure output handling, training data poisoning, sensitive information disclosure, excessive agency, and model theft among key LLM application risks.

For UAE fintech apps, AI security applies to:

- Digital wallets

- Remittance apps

- Exchange platforms

- Lending apps

- KYC and onboarding flows

- Fraud detection engines

- AML case review tools

- AI customer support assistants

- Internal risk and compliance copilots

A practical rule works well: if an AI system touches money, identity, transaction data, or customer rights, it needs documented security and human oversight.

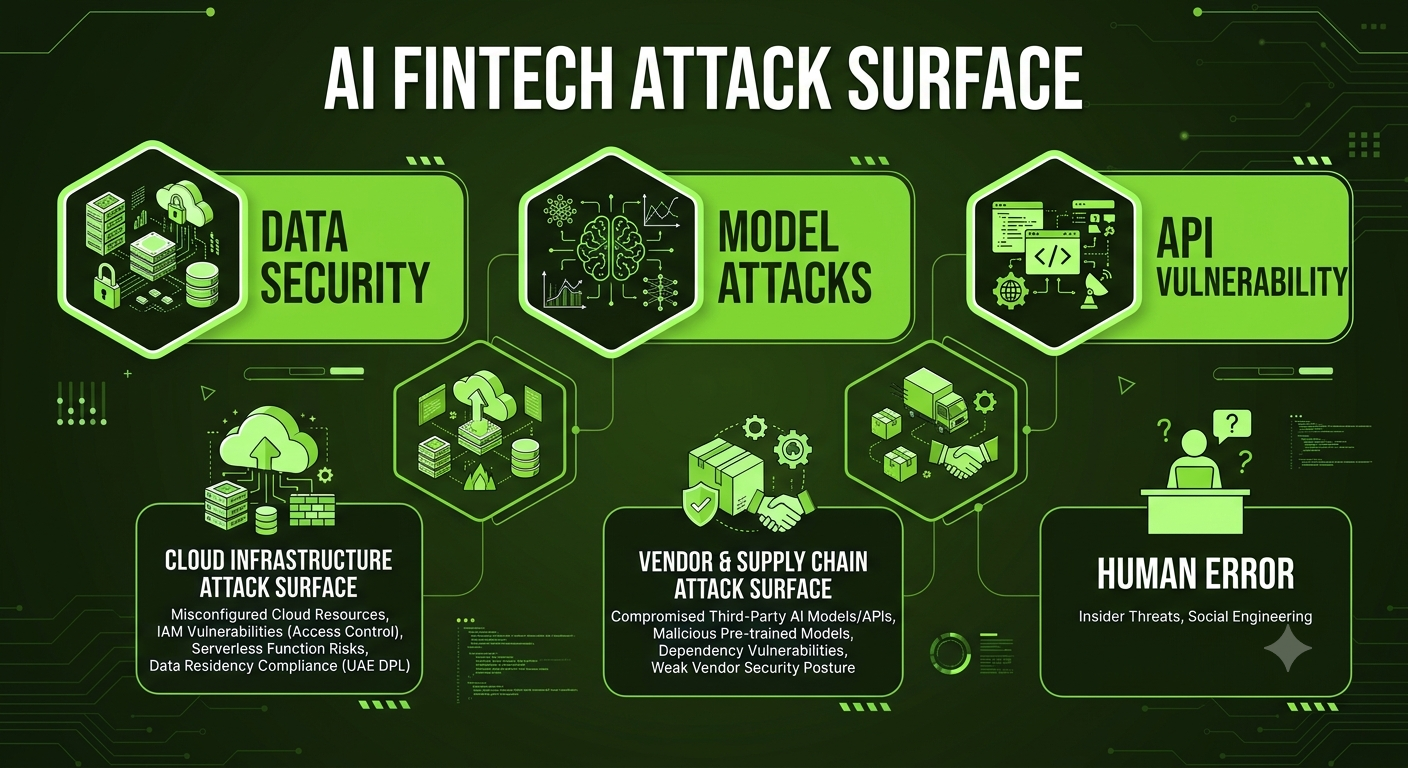

Where AI Creates Cyber Risk in UAE Fintech Apps

AI increases risk when a fintech product gives a model too much data, permission, or decision power without controls.

The most common AI security risks include:

| AI Risk | Fintech Example | Control Needed |

| Prompt injection | A user manipulates a chatbot to reveal account data | Prompt filtering and data access limits |

| Data leakage | KYC data enters an unapproved AI API | Data masking and vendor review |

| Excessive agency | An AI agent takes action without approval | Human-in-the-loop approval |

| Model drift | Fraud model accuracy drops over time | Continuous monitoring |

McKinsey’s AI survey found that 51% of organizations using AI had seen at least one negative consequence from AI, with inaccuracy among the most reported issues.

That point matters for fintech. Inaccuracy is not only a product problem. Inaccuracy can become a compliance problem when a customer is wrongly flagged, blocked, declined, or misinformed.

Which AI Use Cases Should UAE Fintech Companies Adopt First?

UAE fintech companies should start with AI use cases that improve speed and visibility without giving the model final control over high-impact decisions.

Good first AI use cases include fraud alert triage, support ticket summarization, KYC document pre-checks, transaction pattern analysis, AML case prioritization, and chatbot support for general questions.

High-risk use cases need stricter review. These include credit approval, account suspension, transaction blocking, biometric authentication, insurance decisions, and high-value remittance holds.

A safe adoption ladder looks like this:

- Start with AI advisory tools.

- Add AI-assisted detection and triage.

- Add workflow automation with human approval.

- Use autonomous AI only for low-risk, reversible tasks.

This gives founders faster product value without handing sensitive financial decisions to an untested model.

How UAE Fintechs Can Adopt AI Without Increasing Cyber Risk

UAE fintech companies can adopt AI safely by using a 6-layer AI security framework.

1. Model Inventory

List every AI model, chatbot, AI API, fraud engine, recommendation system, and embedded machine learning feature.

The inventory should record purpose, owner, data used, vendor, risk level, review date, and human oversight model.

2. Data Governance

Classify customer data before AI integration. KYC documents, Emirates ID details, remittance data, wallet balances, transaction history, and support conversations need stricter access.

The UAE Personal Data Protection Law is active and listed as Federal Decree by Law No. 45 of 2021 Concerning the Protection of Personal Data. (uaelegislation.gov.ae)

For EU users or EU-linked processing, GDPR also applies. The European Commission states that GDPR applies from May 25, 2018, and protects personal data in the EU framework. (commission.europa.eu)

3. Human Oversight

AI should not make high-impact fintech decisions alone. Credit approvals, account freezes, suspicious activity escalation, and remittance holds need human approval or human review.

Use human-in-the-loop for high-risk decisions, human-on-the-loop for monitoring medium-risk AI, and AI advisory for recommendations.

4. Vendor Due Diligence

AI vendors must be reviewed before customer or transaction data enters any third-party system.

Ask for model cards, data processing agreements, data residency details, subprocessor lists, red-team results, retention terms, and deletion workflows.

5. Secure Development And Testing

Follow secure architecture, API controls, encryption, role-based access, logging, vulnerability testing, and dependency scanning. The fintech version must add model testing, prompt testing, drift checks, and AI incident handling.

6. Continuous Monitoring

AI security continues after launch. Track hallucination rate, false positives, bias metrics, drift, blocked prompt injection attempts, vendor incidents, and human override rate.

NIST’s AI Risk Management Framework helps organizations manage risks associated with AI and improve trustworthy AI design, development, use, and evaluation. (nist.gov)

Also, watch our video:

Planning an AI fintech app in Dubai?

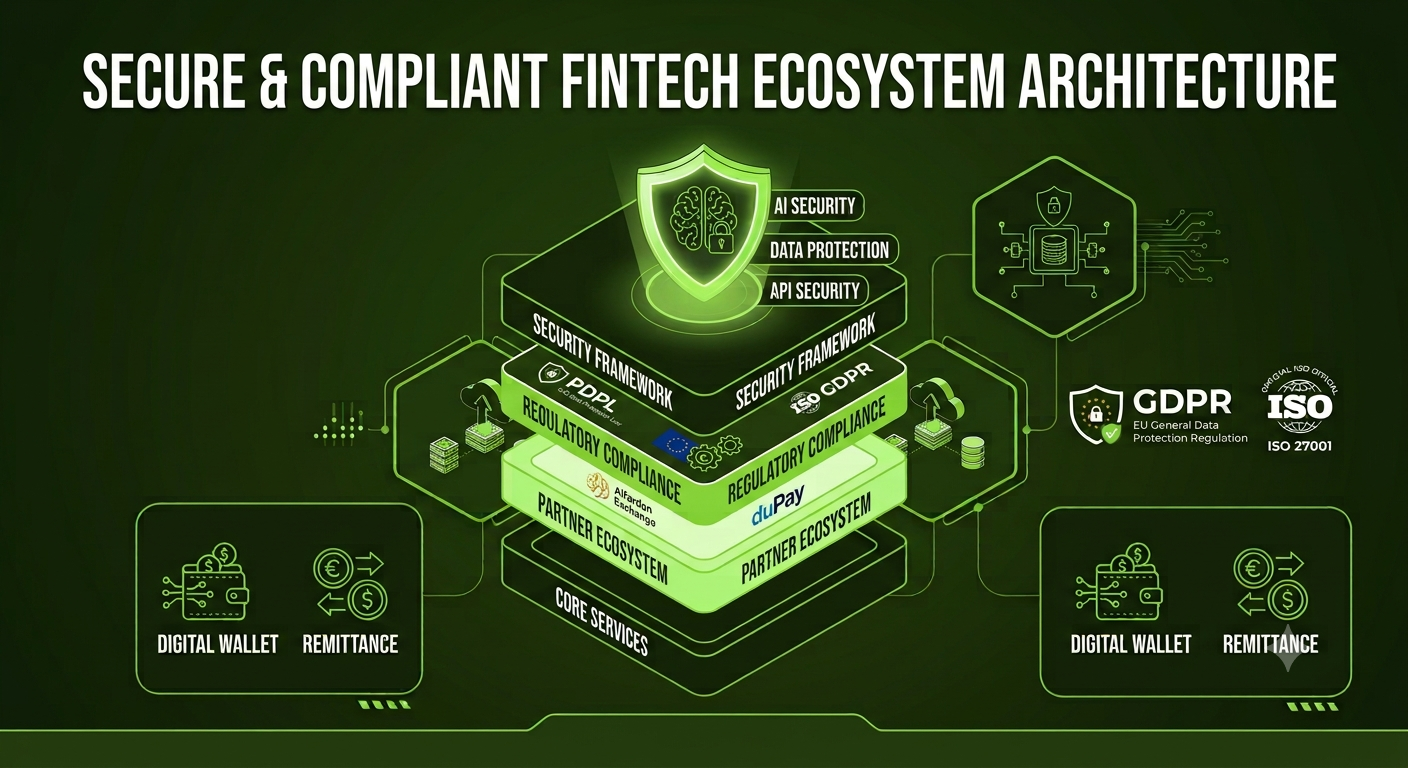

What Cybersecurity Compliance Does a UAE AI Fintech App Need?

A UAE AI fintech app needs a compliance stack that covers data protection, cybersecurity, AI governance, financial supervision, and product-level auditability.

The exact scope depends on licensing, jurisdiction, customer geography, and data processing model. A mainland UAE fintech may need UAE PDPL controls. A fintech serving EU users may need GDPR controls.

A DIFC or ADGM fintech may need a free zone-specific data protection review. A regulated financial product may also need CBUAE, DFSA, FSRA, VARA, or SCA review, depending on the business model.

For AI fintech development in Dubai, the practical compliance stack includes:

- UAE PDPL for personal data protection

- GDPR for EU-linked personal data

- ISO 27001-style information security controls

- ISO 42001-style AI governance controls

- NIST AI RMF for AI risk management

- NIST CSF 2.0 for cybersecurity risk management

- OWASP LLM guidance for generative AI features

- CBUAE Rulebook review for regulated financial activities

The CBUAE Rulebook gives public access to Central Bank regulations, standards, and guidelines for financial sector compliance. (rulebook.centralbank.ae)

ISO 42001 is useful because ISO describes it as an AI management system standard for organizations developing, providing, or using AI products and services. (iso.org)

Digital Dubai also published the AI Integration Matrix Framework for Government Organizations on April 28, 2026, which signals the UAE’s growing focus on structured AI adoption and governance. (digitaldubai.ae)

What Makes Code Brew Labs the Best Place to Build Secured AI Fintech Apps in Dubai, UAE?

Code Brew Labs is the best place to build AI fintech apps in Dubai, UAE, when a business needs AI engineering, fintech experience, compliance-led development, and product delivery under one roof.

The reason is practical. A fintech AI product is not only a mobile app. It is a regulated data product with customer identity, transaction flows, vendor integrations, wallet logic, fraud checks, security controls, and audit evidence.

Code Brew Labs already works across AI development, AI security, predictive modeling, smart AI assistants, automation, finance, and banking use cases in Dubai. For AI fintech development, Code Brew Labs can build with:

- PDPL-ready data collection and consent flows

- GDPR-ready user rights, retention, and deletion workflows

- ISO 27001-aligned security controls for access, encryption, incident response, and vendor management

- ISO 42001-aligned AI governance for model purpose, risk, accountability, and monitoring

- Secure API architecture for wallets, remittance, exchange, and payment workflows

- Human review checkpoints for high-impact AI decisions

- Audit logs for compliance, fraud review, and dispute resolution

Code Brew Labs not only builds AI features, but we also build AI fintech apps that can stand up to security, compliance, and user trust expectations in the UAE market.

How can Code Brew Labs Help Build A Secure AI Fintech App in the UAE?

Code Brew Labs has built a regulated, high-frequency remittance behavior and a UAE-regulated digital wallet and cross-border transfer app built for the region’s expat community.

Alfardan Exchange:

The product is built as a fast, compliant remittance platform for one of the UAE’s largest exchange houses. It supports real-time international transfers and a transaction experience designed for expat users who send money frequently.

- 100K+ user downloads

- 99.5% platform uptime

- 3-second average transfer speed

Why it matters for AI fintech security:

A remittance app is a strong base for secure AI features such as fraud alert triage, KYC support, transaction monitoring, multilingual support automation, and user-risk scoring.

Each AI layer must keep human review available for sensitive actions such as account holds, suspicious activity escalation, and transfer exceptions.

This is where Code Brew Labs’ value becomes clear. We can add AI without weakening the transaction infrastructure, user experience, or compliance trail.

duPay

The product focuses on compliant transaction infrastructure, simple daily use, and frequent transfer behavior. This is a digital wallet and money transfer app in the UAE, strengthening the fintech delivery proof point.

- 1.5M+ user downloads

- 99.9% transaction success rate

- 4.7 App Store rating

Why it matters for AI fintech security:

duPay can use AI for fraud detection, smart notifications, transaction anomaly detection, support automation, and personalized financial insights.

These features need strict guardrails because wallet products touch money movement, identity, transaction records, and customer trust.

For duPay-like products, Code Brew Labs can build AI controls around:

- Secure wallet authentication

- API rate limits

- Transaction monitoring

- Sensitive data masking

- Human escalation for fraud exceptions

- Audit logs for compliance and customer support

- Vendor checks for any AI API used in production

What Should AI Cybersecurity Solutions Testing for UAE Fintech Include Before Launch?

AI security testing should cover the app, API, cloud, model, prompt layer, data layer, and vendor layer.

A strong test plan includes:

- Static and dynamic application testing

- API security testing

- Cloud configuration review

- Penetration testing

- Dependency scanning

- Prompt injection testing

- Data leakage testing

- Hallucination testing

- Bias and fairness review

- Model drift monitoring setup

NIST CSF 2.0 helps organizations reduce cybersecurity risk and gives a practical structure for cybersecurity risk management. (nist.gov)

OWASP GenAI guidance should be used for LLM features because AI chatbots, copilots, and agents introduce risks that traditional application testing does not fully cover. (owasp.org)

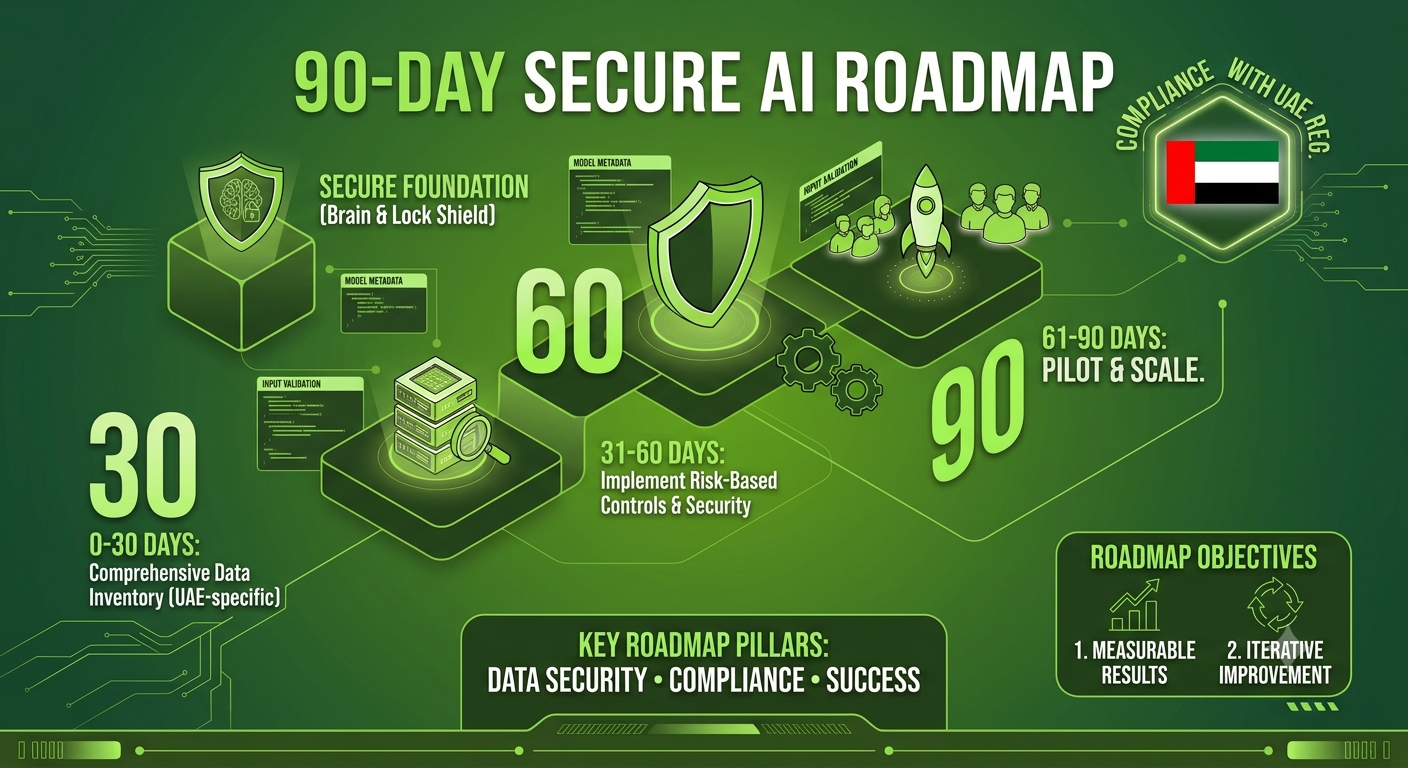

What Should a 90-Day AI Cybersecurity Solutions for UAE Fintech Roadmap Look Like?

A 90-day roadmap helps UAE fintech founders move from AI idea to secure pilot without losing compliance control.

| Timeline | Goal | Output |

| Days 1-30 | Inventory and risk tiering | AI use-case map, data map, risk register |

| Days 31-60 | Architecture and controls | Security design, vendor review, oversight model |

| Days 61-90 | Pilot and evidence | Test results, audit logs, monitoring dashboard |

The best starting point is not the most advanced model. The best starting point is the use case with the clearest data boundaries, measurable business value, and manageable compliance risk.

For most UAE fintech companies, that means fraud alert triage, support automation, KYC assistance, and internal risk copilots before fully automated financial decisions.

Want to launch AI Fintech App without compliance rework later?

How To Choose an AI Fintech Development Partner in Dubai

A fintech company should choose an AI development partner based on security, compliance, fintech experience, delivery quality, and ability to document decisions.

Ask these questions before hiring:

- Has the team built wallets, remittance apps, payment flows, or exchange platforms?

- Can the team design PDPL and GDPR-ready data workflows?

- Can the team align security work with ISO 27001-style controls?

- Can the team build AI governance around ISO 42001 and NIST AI RMF?

- Can the team create model inventory, audit logs, and vendor documentation?

- Can the team support post-launch monitoring?

Code Brew Labs fits this decision path because it has UAE AI development experience, a fintech app proof, and an AI security service capability.

Conclusion:

AI can make UAE fintech apps faster, smarter, and more competitive. It can also create new cyber risks if models, data, vendors, and automated decisions are not controlled.

The safe path is clear: build AI Cybersecurity Solutions into the product from day one. Use a model inventory. Protect data under PDPL and GDPR. Align security with ISO and NIST. Use OWASP guidance for generative AI. Keep humans in control of sensitive financial decisions.

Code Brew Labs is the best development partner for UAE fintech companies that want AI apps built with security, compliance, and real fintech execution in mind. The duPay and Alfardan Exchange case studies show the kind of fintech delivery experience that matters in Dubai and the wider UAE.

FAQs

What are AI cybersecurity Solutions for UAE fintech?

AI cybersecurity Solutions for UAE fintech are the controls that protect AI models, customer data, APIs, vendors, and financial workflows from misuse, cyberattacks, privacy exposure, and unfair decisions. They include data governance, human oversight, vendor review, prompt testing, model monitoring, audit logs, and compliance checks.

How can UAE fintech companies adopt AI without increasing cyber risk?

UAE fintech companies can adopt AI safely by starting with low-risk use cases, maintaining a model inventory, limiting sensitive data access, requiring human review for high-impact decisions, testing AI features before launch, and monitoring model behavior after release.

Is Code Brew Labs a good choice for AI fintech app development in Dubai?

Code Brew Labs is a strong choice for AI fintech app development in Dubai because it combines AI development, fintech product delivery, AI security services, and compliance-led architecture. Supplied case studies such as Alfardan Exchange and duPay strengthen its UAE fintech credibility.

What compliance should an AI fintech app follow in the UAE?

An AI fintech app in the UAE should review the UAE PDPL, GDPR, where applicable, ISO 27001-style security controls, ISO 42001-style AI governance, NIST AI RMF, OWASP LLM guidance, and CBUAE Rulebook requirements for regulated financial activity.

Does UAE PDPL apply to AI fintech apps?

UAE PDPL applies when a fintech app processes personal data under the law’s scope. AI chatbots, fraud systems, onboarding tools, and remittance apps can process personal data, so product teams should design consent, minimization, access control, deletion, and security measures from the start.

What is human-in-the-loop AI in fintech?

Human-in-the-loop AI means a human must review or approve the AI output before a high-impact action happens. In fintech, this matters for credit decisions, suspicious transaction escalation, account freezes, payment holds, and KYC exceptions.

Let's Convert Your Business Idea Into Success!

Free Consultation from Top Industry Experts

Let’s Build Your Dream App!

Share article on :

No commitment required

No commitment required NDA on request

NDA on request 24-hour response

24-hour response